I know that many of you may be rolling your eyes when somebody brings up a topic about pension. It often feels like a dry, distant topic — something for "future you" to worry about. But in the UK, understanding how they work is one of the most effective ways to build wealth for the future you and reduce your tax burden - especially if you're a higher rate tax payer (check my UK tax system guide for more on tax brackets).

In this first part of my pension guide, I want to cover the basics of the UK pension system and break down the three main types of pensions.

The Three Pillars of the UK Pension System

The UK pension landscape is built on three main components. Most expats will interact with at least two of these during their time in the country.

1. The State Pension (The Safety Net)

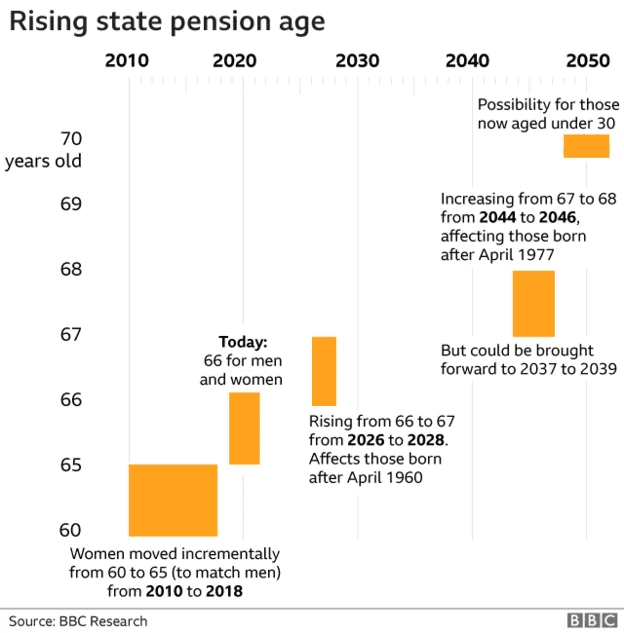

The State Pension is a monthly payment from the government once you reach the state pension age (currently 66, rising to 67 and 68 in the future). It is not "pot-based" — you don't have a personal account with your name on it. Instead, it is funded by current National Insurance (NI) contributions.

Key Rules:

- Minimum 10 years: You need at least 10 qualifying years of NI contributions to get any state pension.

- Full Pension (approx. 35 years): To receive the maximum amount, you typically need 35 qualifying years.

- Age: Paid starting from age 66–68 depending on when you were born.

Important nuance for expats: Your qualifying years do not have to be consecutive. Furthermore, depending on where you moved from, you might be able to combine your UK years with social security years from other countries (like the EU or countries with reciprocal agreements) to meet the 10-year minimum.

The age at which people can start claiming state pension has been rising over the years. If you were to retire in 2010 women could start getting pension at the age of 60 and men at 65. As of today, it's 66 and the numbers are rising.

By the time I qualify for a state pension, I’ll likely be well into my 70s. It’s hard to picture myself calmly finishing my avocado on toast and then squeezing onto the Tube during rush hour to head into the office. And who knows—by then, advances in medicine might extend our lifespans even further, giving governments an excuse to push the pension age to 150. It’s not impossible to imagine a future where the whole idea of a state pension is completely rethought — or even scrapped altogether.

Therefore, in my view, it’s essential to build a pension of your own — one you actively contribute to and have control over, whether that’s through a workplace scheme or a personal pension like a SIPP.

2. Workplace Pensions

Since 2012, the UK has had Automatic Enrolment. If you are aged between 22 and the State Pension age and earn more than £10,000 a year, your employer must automatically sign you up for a workplace pension. More of that rules you'll find in Joining a workplace pension guide.

This is the most common way expats save for retirement. You contribute a slice of your salary, and your employer is legally required to add to it.

The minimum contributions: Most companies follow the legal minimums:

- 5% Employee contribution (taken from your pay)

- 3% Employer contribution (added by your company)

You don't usually get to choose the provider for your workplace pension—your company does. You’ll likely see names like Aviva, The People’s Pension, Scottish Widows, etc.

Qualifying Earnings Trap

Here is a crucial detail many people miss. The 3% employer contribution is usually calculated on "Qualifying Earnings", not your entire gross salary.

Qualifying Earnings Band (2025/26)

| Earnings Tier | Annual Amount | Employer Contribution |

|---|---|---|

| Lower Threshold | £0 – £6,240 | £0 (No contributions) |

| Qualifying Band | £6,240 – £50,270 | 3% Minimum |

| Upper Cap | Above £50,270 | £0 (Unless on full salary) |

This means they only pay 3% on the portion of your earnings between £6,240 and £50,270 (for the 2025/26 tax year).

For example, if you earn £100,000, your employer's 3% contribution isn't £3,000—it's actually 3% of (£50,270 - £6,240), which is around £1,320. In this case, the effective contribution rate is closer to 1.3%, not 3%. Always check if your employer offers to pay on your full salary instead; this is a common "perk" in better benefit packages.

The magic of the employer match

Why do people call pensions "free money"? Because of the Employer Match.

Imagine you decide to contribute £200 a month to your pension. If your employer offers a 1:1 match, they will also put £200 in. Suddenly, £400 is going into your investment pot, but it only cost you £200 of your gross pay. That is an instant 100% return on your money before it's even invested in the stock market.

Reality Check: While the "match" is powerful, its generosity varies. Many startups and smaller companies stick strictly to the legal minimum of 3%. "Generous" matches—where an employer might match up to 5%, 8%, or even 10%—are becoming rarer outside of Big Tech, Finance, or older corporate institutions. My advice - always take the maximum match your employer offers; otherwise, you are effectively turning down a part of your salary.

3. Personal/Private Pensions

These are pensions you set up yourself, independent of your employer. They are particularly useful for the self-employed or those who want more control over their investments. We will dive deep into SIPPs (Self-Invested Personal Pensions) in Part 2 of this guide, but you can also look into other UK investment options for beginners if you're just starting out.

Understanding the Tax Mechanics: Net Pay vs. Relief at Source

This is where it gets technical—and where many people lose money without realising it. There are two main ways your pension contributions are handled for tax purposes.

| Method | How it works | Impact on Higher Rate Taxpayers |

|---|---|---|

| Gross Basis | Money is taken before tax is calculated. | You get full 40% tax relief automatically. |

| Net Basis - Relief at Source | Money is taken after 20% tax is applied. | You only get 20% relief automatically. |

So, if you are a higher rate tax payer, please check you Workplace policy - if it says Net Basis / Relief at source, it means that you're getting back only 20% automatically. You need to call HMRC or fill in a Self-assessment tax return to claim back the missing 20%. When to claim? For the best management of your tax, you can make a claim annually, but you have a limit of up to 4 years to backdate it.

What is Salary Sacrifice?

If your employer offers "Salary Sacrifice" for pensions, say yes.

In this setup, you technically "give up" part of your salary before you receive it, and the employer puts that amount into your pension as an employer contribution. Because your official salary is now lower, both you and your employer pay less National Insurance (NI). It is the most tax-efficient way to contribute to a pension in the UK.

Conclusion

The UK pension system is designed to reward those who start early and take advantage of employer contributions. In the next part of this guide, we will look at how to take total control of your pension with a SIPP and how high earners can use pensions to avoid the dreaded 60% tax trap.

Take your employer match, check if your tax relief is being applied correctly, say 'yes' to salary sacrifice if offered. To understand how pensions fit into your overall monthly budget in London, check our cost of living guide. Importantly, negotiate! If not extra numbers to you salary, why not to negotiate other sides of compensation package? For example, when accepting the job offer, ask your employer to contribute to your full salary, not just qualifying earnings or to contribute a higher percentage.

Next Step: Read Part 2: SIPP and Pension Tax Strategy to learn how to optimize your retirement savings for maximum tax efficiency.

Disclaimer: I am not a financial advisor. This information is for educational purposes only. Pension rules and tax laws change; always consult a professional or official GOV.UK resources.