If you're a higher-rate or additional-rate taxpayer contributing to a SIPP, you're probably leaving money on the table. Your pension provider only claims the basic 20% tax relief automatically — but you're entitled to more. This guide shows you exactly how to claim that extra tax relief from HMRC, when to do it, and what to expect.

How SIPP pension tax relief works

When you contribute to a SIPP (Self-Invested Personal Pension), your provider automatically adds basic-rate tax relief to your contributions. If you put in £800, they claim £200 from HMRC and your pension pot receives £1,000. This happens regardless of your tax band.

But here's what many people miss: if you pay tax at a higher rate, you're entitled to additional relief that doesn't come automatically.

| Tax band | Rate | Auto relief | You must claim |

|---|---|---|---|

| Basic rate | 20% | 20% | Nothing |

| Higher rate | 40% | 20% | Extra 20% |

| Additional rate | 45% | 20% | Extra 25% |

For higher-rate taxpayers, this means on a £10,000 gross contribution (£8,000 net), you can claim back £2,000 from HMRC. For additional-rate taxpayers, it's £2,500. Over a career, this adds up to thousands of pounds.

If you're not sure which tax bracket you fall into, check your payslip or P60. The higher rate kicks in at £50,270 of taxable income for the 2025-26 tax year.

When to claim your pension tax relief

This is a question that guides hardly ever mention — when exactly should you submit your claim?

The simplest approach: claim once the tax year ends. If you contributed to your SIPP before 5th April 2026, you can submit your tax relief claim for the 2025-26 tax year starting from 6th April 2026.

You don't need to wait until January or file a full Self Assessment tax return. If you're a PAYE employee with no other income sources (rental income, self-employment, etc.), you can use HMRC's dedicated relief claim form instead — it's faster and simpler.

Important timing notes:

- You can claim for the previous 4 tax years, so don't panic if you've missed past years

- Claims made early in the tax year (April-June) tend to be processed faster

- Keep records of all your contributions — you'll need them as proof

Step-by-step: how to claim pension tax relief from HMRC

Here's the process for claiming your extra relief online.

What you'll need before starting

As HMRC's guidance states, gather these documents first:

- your National Insurance number

- the type of pension and name of the pension provider

- the net amount of pension contributions for each tax year you're claiming for

- your payroll number (if doing for workplace pension) or reference number (for SIPPs)

- a proof - e.g. letter or statement from your pension provider

Most SIPP providers (Vanguard, AJ Bell, Hargreaves Lansdown, Interactive Investor) provide annual statements that work as proof. Download these from your account before you start.

Submitting your claim

Step 1: Go to the HMRC claim page: gov.uk/guidance/claim-tax-relief-on-your-private-pension-payments

Step 2: Scroll down and click the "Claim now" button.

Step 3: Log in to your Government Gateway account. If you don't have one, you'll need to create it first — this takes about 10 minutes and requires your National Insurance number.

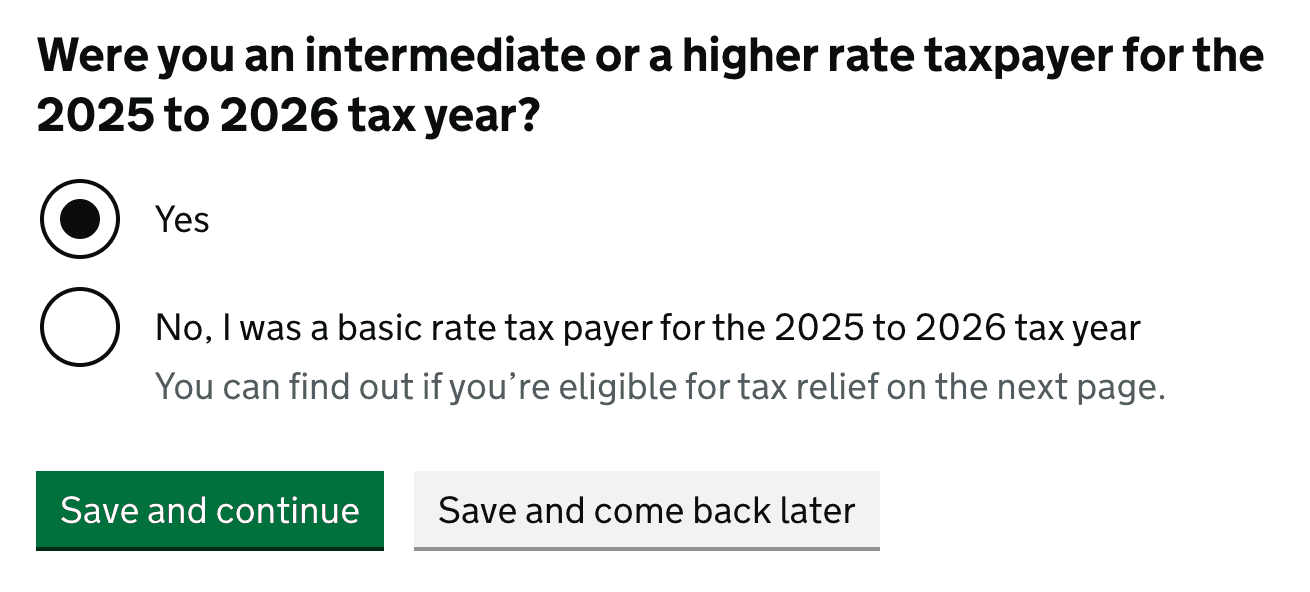

Step 4: Work through the form. It will ask which tax year you're claiming for and confirm your taxpayer status.

Step 5: Enter your contribution amounts and upload your proof documentation.

Step 6: Review and submit. You'll receive a confirmation reference — save this.

How HMRC pays your tax relief

Once your claim is processed, HMRC will return your money in one of three ways:

- Cheque — posted to your registered address

- Bank transfer — paid directly to your bank account (increasingly common)

- Tax code adjustment — your tax-free allowance increases for the following year, meaning you pay less tax each month

If you prefer a lump sum, you can request this when submitting your claim. The tax code adjustment spreads the benefit over 12 months, which some people prefer for budgeting.

How long does HMRC take to process claims?

Processing times vary, but expect:

- Simple claims (single year, clear documentation): 4-8 weeks

- Multiple years: 2-3 months

- Complex cases (missing documentation, queries): up to 6 months

Claims submitted early in the tax year (April-June) typically process faster than those submitted during Self Assessment season (January-March) when HMRC is busiest.

You can check your claim status through your Personal Tax Account on GOV.UK.

Common mistakes to avoid

Not claiming at all — Many higher-rate taxpayers simply don't know they're entitled to extra relief. If you have a SIPP and pay 40%+ tax, you almost certainly have money to claim.

Waiting too long — You can only go back 4 years. If you started your SIPP in 2020 and haven't claimed, some of that relief may be lost forever.

Wrong contribution figures — Use the net amount you contributed (what left your bank account), not the gross amount shown in your pension. Your provider statement will clarify this.

Missing documentation — HMRC may reject or delay claims without proper proof. Always attach your provider statement.

What if you do Self Assessment?

If you already file a Self Assessment tax return (because you're self-employed, have rental income, or earn over £150,000), you should claim pension relief through your tax return instead of the separate form.

In the Self Assessment, there's a section for pension contributions. Enter your net contributions there, and HMRC calculates your relief automatically. This is actually simpler than the standalone claim process.

What if I contribute monthly?

Many people set up a standing order to contribute a fixed amount to their SIPP each month. If that's you, should you claim relief after each contribution?

No — wait until the tax year ends and submit one claim for the whole year. Here's why:

HMRC's form is designed for annual claims. It asks for your total contributions per tax year, not monthly breakdowns. Submitting 12 separate claims would be tedious and likely cause confusion.

Your provider's annual statement is the easiest proof. This document summarises all your contributions for the tax year in one place. Claiming mid-year means gathering multiple statements or bank records instead.

There's no benefit to claiming early. Unlike some tax matters, there's no interest or penalty for waiting. The relief amount is the same whether you claim in April or the following January.

Practical approach: Set up your monthly contributions, let them accumulate throughout the year, then in April (after the 5th) download your annual statement from your SIPP provider and submit one claim for the full year's total.

Keeping records for future claims

Good record-keeping makes future claims painless. Create a simple folder (physical or digital) for each tax year containing:

- Annual statement from your SIPP provider

- Bank statements showing the transfers to your pension

- Confirmation emails from your provider when contributions were received

- Your claim confirmation reference from HMRC

Most providers let you download statements as PDFs. Do this each April when the tax year ends, while everything is fresh. If HMRC ever queries a claim, you'll have everything to hand.

Next steps

Now that you know how to claim your SIPP tax relief, make sure you're maximising your pension strategy overall. Read my SIPP and pension tax efficiency guide to understand contribution limits and how pensions help you avoid the 60% tax trap.

If you're still building your financial foundation in the UK, you might also want to explore ISAs and other tax-efficient investments — they complement pensions well for medium-term goals.